Through Jared dillian

Inflation trade took a shovel last week as the Federal Reserve pondered aloud about perhaps raising interest rates a little earlier.

That’s it. That’s all that happened.

There are a few lessons here.

- We have inflation, and the Fed’s statements are an unspoken admission that inflation is not transitory. If it were truly transitional, there would be no need to accelerate rate hikes.

- It will take much more than words to derail this inflationary impulse. He will take action. Words have power, but the Fed must in fact do something lower inflation, such as raising rates or reducing asset purchases, and that’s still a long way into the future.

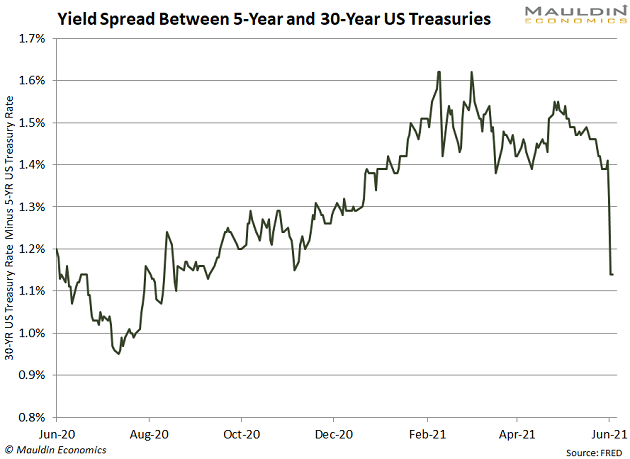

- I was not surprised that the Fed changed its stance on monetary policy. If you’ve been paying attention to speeches and statements from the past month, it was clear that inflation was at the center of the Fed’s concerns. What surprised me was the market reaction, which was violent in relation to the tiny change in expectations. There is a lot of influence in the system and a lot of cluttered positions. You can see it on this graph of the yield curve, expressed as the difference between the five-year and 30-year rates.

Inflation isn’t dead, just because the Fed says so. He’s alive and well, and the Fed is going to have to work really hard to kill him.

My trip to Greece

I have just returned from vacation in Greece, and I have some knowledge of macroeconomics.

The dollar is very strong.

Granted, it’s Greece, and things are cheaper there, but I had dinner for two in Milos for EUR 30, or around $ 36. With enough food for us to take the leftovers to the hotel in bags. It was even cheap in Athens, and the notoriously expensive Santorini wasn’t that bad.

Even after the big move this year and last year, the dollar is not particularly weak. In purchasing power parity, it has the possibility of weakening further.

There is also the question of the wisdom of combat tendencies. I wouldn’t characterize the weak dollar trend as relentless, but it has been a constant feature of the markets for about a year. Betting on a stronger dollar is like fighting against a very strong trend. You first.

Monday’s price action indicates that inflation trading and the dollar’s weaker trend are going to be very hard to kill.

It also reminded me of the European Central Bank, which has no intention of exiting negative rates at the moment. If so, the movement of EURUSD could be quite extreme.

There are a lot of trades to be done if you think rates are going to rise in Europe. Most of them are pretty obvious.

Without going into much detail (and political opinions), I returned home on Sunday very optimistic about Europe. The United States is the global center of innovation, but we don’t have a monopoly on savings, hard work, and savings. It exists elsewhere in the world.

In fact, you could argue that the stocks that have contributed to bumper markets (and asset prices) in the United States are deteriorating and improving elsewhere. We should all have a higher allocation to foreign stocks.

Victory towers

Have you ever noticed that everything in finance is also political?

Conservatives love gold; the Liberals love paper.

Conservatives love value stocks; liberals like growth stocks.

The Conservatives are betting on inflation; the liberals are betting on deflation.

These are largely political arguments, not financial arguments. People believe anything that confirms their background. After the FOMC meeting, when inflation trading was hammered home, liberals who had been battling inflation trading for the past seven months saw trade move in their favor for a day and took a ride of victory.

I also came back from Greece rather disappointed by Twitter– even debates about money are about politics.

I’m a right-wing man (economically speaking), so I believe in gold, value stocks, and inflation. Here’s how finance (and politics) work: you win for a while, then I win for a while.

Left-wing investors have had a monopoly on good ideas over the past 10 years. Now they’re experiencing a bit of cognitive dissonance that their psychological model is no longer working.

I recently saw that the average value rotation lasts 64 months. We are currently in month number seven. This is going to go on for a while and cause a lot of frustration for some.

Richard Russell once said that a bull market is actually a bull – it tries to get rid of as many riders as possible. I saw the collapse of inflation from my Bloomberg app on my phone in Greece. It didn’t spoil my day. Not too many bad days in Santorini.

If you’ve been wrong for seven months on anything, it might be a good idea to do a little soul-searching.

Originally published by Mauldin Economics, 06/24/21