serves/E+ via Getty Images

The iShares MSCI Germany ETF (NYSEARCA: EWG) is an exchange-traded fund offering investors exposure to German mid- and large-cap stocks. The German stock market is not as developed as, say, the US stock market. As a result, the fund holds relatively few assets, 61 as of May 26, 2022. The level of concentration is not too high, although the top 10 holdings represented approximately 52.54% of the portfolio as of May 26, 2022. The fund’s expense ratio is 0.50% (not particularly cheap), while assets under management stood at $1.69 billion as of May 27, 2022.

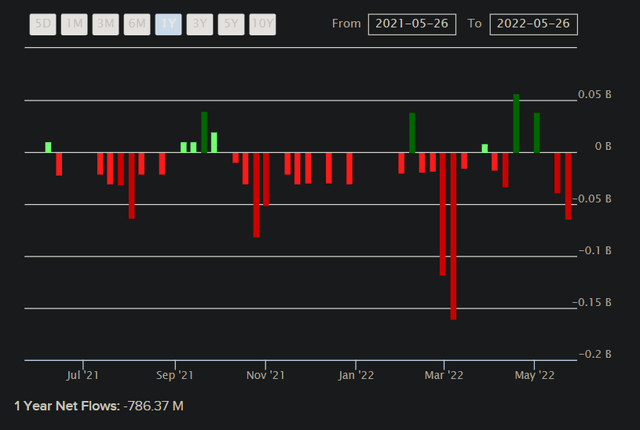

Assets under management of $1.69 billion follows a year of net outflows of approximately $786 million, as illustrated in the chart below.

ETFDB.com

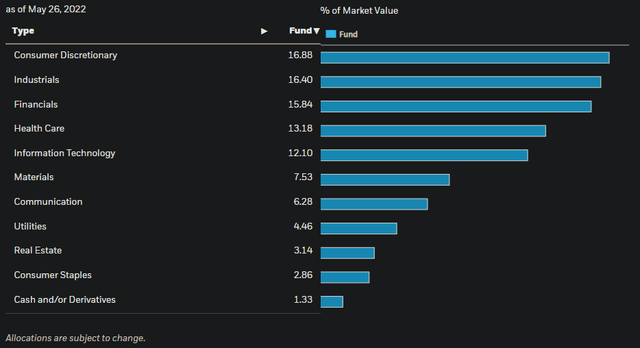

European stocks are not known for strong earnings growth and business productivity. Nevertheless, all equity funds can be rated and offer good value from time to time. Some mature, developed and economically sophisticated economies, particularly in Europe, can often be made up of quite low yielding and “heavy” sectors such as finance and real estate. There is some of that in EWG, but the portfolio has a good level of exposure to consumer discretionary, industrials and technology; a mix of cyclical and economically sensitive sectors that give EWG a chance to outperform.

iShares.com

The fund seeks to track its benchmark, the MSCI Germany index. As of April 29, 2022, the index had a price-to-earnings ratio of 14.03x, a forward price-to-earnings ratio of 11.06x, and a price-to-book ratio of 1.47x. The dividend yield was 3.42%, implying a dividend payout rate of around 48% (let’s call it 50%), and an implied expected return on equity of 13.3% (reasonably good; not close best-performing US companies, but better than some low-performing countries like Japan).

Given the duration of the rates in Germany (the current rate 10 years bond yield is less than 1.0%), I would say that the forward price/earnings ratio is fundamentally too low. The implied return on expected earnings is around 9%, so removing the 1% 10-year rate as a proxy for the risk-free rate would reveal an underlying equity risk premium of 8%. It’s not the long-term equity risk premium, but it’s a start. If we were to assume stable growth of, say, 2% earnings growth thereafter, and a cost of equity of, say, 1% (risk-free rate) plus an equity risk premium of 5%, the cost of equity would be 6%. Excluding the long-term growth rate of 2%, this would allow us to justify a forward price-earnings ratio of 25x. If we increase the ERP to 6% and the long-term growth rate even to 0%, you are still looking at a multiple of 14.29x. This is higher than EWG’s benchmark leading multiple of 11.06x.

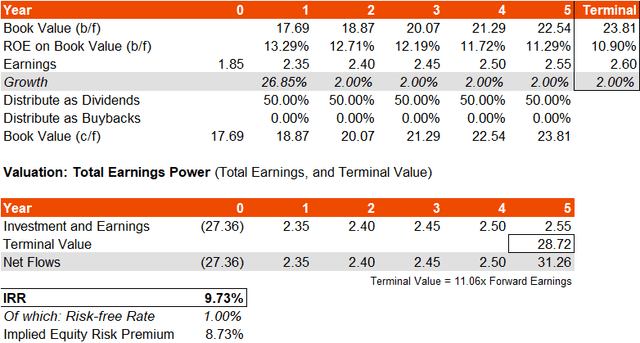

However, assuming no redemptions at this time, and keeping the dividend payout rate constant at 50%, and ROE down towards 10% (but keeping earnings growth at at minus 2% per year after the first year to come), I arrive at following a simple evaluation. the morning star projects 3-5 year earnings growth at an average of 8.34%, while my 3-year average (including MSCI’s projected jump over the next year or so) is 9.69% even with my lower assumption of 2% per year thereafter. My five-year average earnings growth number would be 6.55% though, which is lower than Morningstar’s number, so I think those numbers are about in line with expectations (basically not optimistic or overly pessimistic ).

Author’s calculations

This “valuation” gives me an IRR of 9.73%, with an implied ERP of 8.73%, which is considerably high even with an arguably low forward price/earnings ratio of 11.06x in year five ( for the terminal value number). This assumes no redemption and is based simply on the entire earning power of EWG’s portfolio (based, perhaps, on a less optimistic forecast).

I think 2% earnings growth from year 2 is not unreasonable, which would include inflation, and if we keep that to a minimum, any redemptions (not included in my calculations above) would only serve as a bonus (i.e. our IRR could go up to 14-15% if we were to value EWG based on the equally large dividends and redemptions). But basically, our IRR should be close to 10%, which is very high compared to the low rates in Europe and Germany in particular.

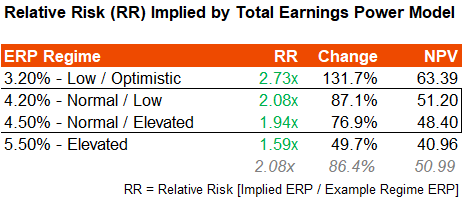

The table below compares my implied equity risk premium of 8.73% to a combination of different ERPs under different regimes. Even under a “high” ERP of 5.50%, EWG probably deserves about a 50% upside in price appreciation.

Author’s calculations

However, it’s possible that a “high” ERP of 5.50% actually makes sense for low-yielding (and less “exciting”) countries like Germany. Although there is a lot of money circulating in the global financial system, capital is ultimately limited, and so equity investors will often favor more exciting and faster growing countries and sectors over less exciting ones, while account done. The fact is that the ERP for Germany may remain high. Still, the IRR is good, and for more risk-averse investors and/or US investors looking for international diversification, German equities still look attractive on a valuation basis. Any positive earnings surprise should also be accompanied by further price appreciation, and I believe that at these levels you should be able to benefit from some expansion in earnings multiples over the longer term (especially if the risk-free rates remain low).